Use our promissory note template to detail the terms of loan repayment.

Updated August 16, 2024

Written by Sara Hostelley | Reviewed by Susan Chai, Esq.

A promissory note records all the terms and conditions of a loan transaction between a borrower and a lender before any money changes hands.

A document used to include collateral in a high-stakes loan.

A document used for quick loans with trustworthy borrowers.

A promissory note is a written promise by a borrower to repay a loan to a lender according to predetermined terms and conditions.

Before the lender provides the requested funds, the lender and borrower should agree upon the loan’s terms, such as the loan repayment schedule, interest rates, and collaterals. Once they agree, they can document the terms accordingly.

After signing the note, the borrower receives the amount promised by the lender and pays back the loan according to the terms. Eventually, the lender will release the borrower from the promissory note once the loan is completely paid off.

Some promissory notes are negotiable, meaning the original payee can transfer the note to another party. However, not all promissory notes are negotiable.

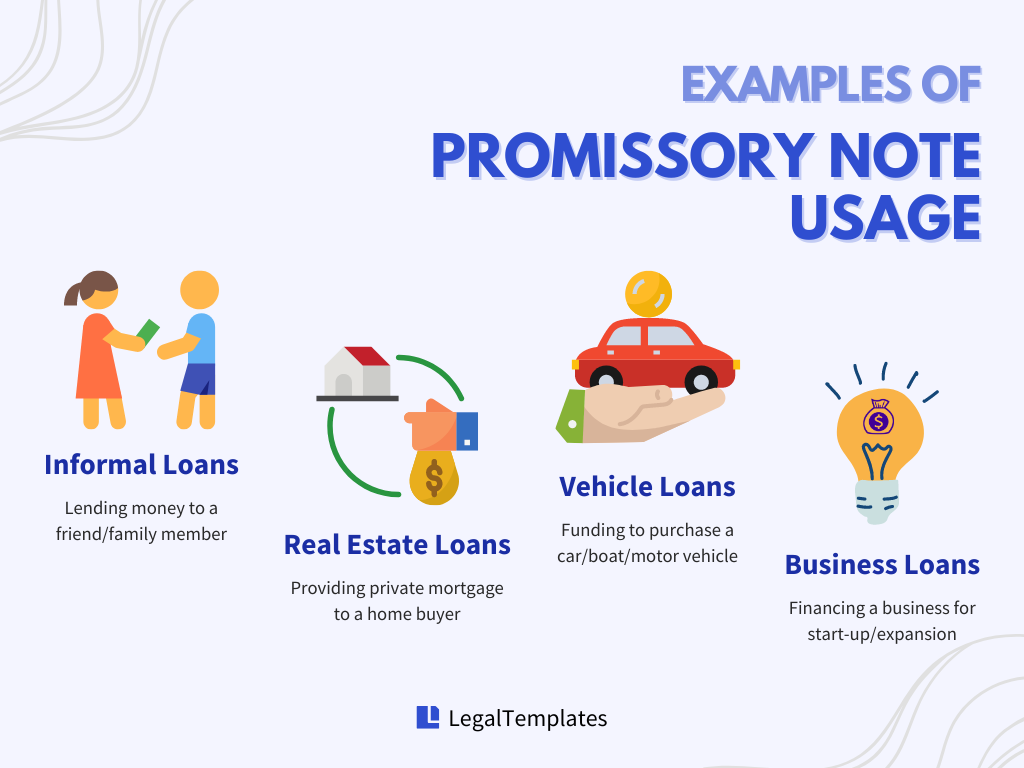

Common scenarios in which you may use a promissory note can include:

Purchase of a Vehicle or Other Item with Financing

Promissory notes are typically for less complex loans or when there is a prior acquaintance between the lender and the borrower. By using promissory notes, lenders ensure legal protection for themselves in the event of a borrower’s failure to return the borrowed money.

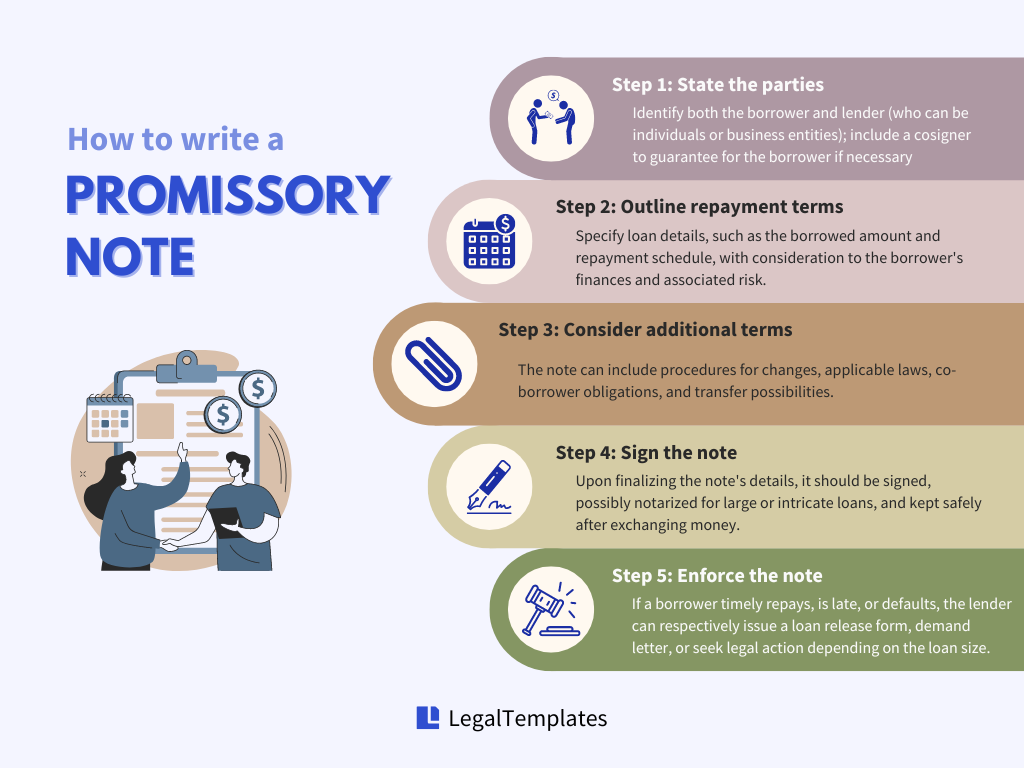

Identify the borrower (the party receiving the loan) and the lender (the party who will be paid back). The parties can be individuals or business entities, such as corporations or LLCs. If either party to the promissory note is a business entity, a representative must sign on its behalf.

If the borrower’s financial stability is questionable, the lender may demand a cosigner with good credit as a safety net for the promissory note.

Consider requesting your borrowers to supply their credit reports for loans.

Borrowers can access these free yearly reports online through websites like AnnualCreditReport.com or credit card company perks. Some online agencies also offer paid financial status checks.

Next, you should clearly outline the following details about the loan and how the borrower will pay it back:

When determining repayment terms and writing the entire agreement, the lender should consider carefully the borrower’s financial condition and the risks associated with the loan. For example, if your borrower has low credit, you may opt for a secured promissory note if the borrower defaults.

Before you complete the promissory note, consider including additional provisions to make your note more comprehensive, such as:

After both the borrower and lender agree to the note’s terms, all parties, including the guarantors if there are any in the arrangement, should sign the note.

Although it’s not legally required, you may consider getting the promissory note notarized if the loan involves a significant amount of money or the terms are complex.

Please only exchange money after the parties sign the note. Furthermore, every party to the note should receive a copy, and the lender should store the original securely.

A copy will suffice if you lose the original. If neither the original nor a copy is present, you may find other ways to prove the agreement’s existence (such as a text exchange). Be aware that the borrower may not have an obligation to repay if there’s no proof that the loan occurred.

Generally, there are three potential outcomes once a promissory note is in effect:

Suppose the borrower pays the total amount per the note’s conditions. In that case, the lender should provide a loan release form to relieve the borrower of any further obligations related to the note.

In case of late payment, the lender must issue a demand letter requesting the full payment and any applicable late fees. If the borrower still fails to make up for the payment, the lender must evaluate the financial viability of initiating legal action.

If the borrower completely defaults on payment, you can enforce it by reminding them of their obligation. If the borrower doesn’t respond or refuses to pay, you can recruit outside help.

For example: John lends $5,000 to his friend Mark, who signs a promissory note agreeing to repay the amount within six months. However, after the deadline passes, Mark fails to repay the loan. John attempts to contact Mark, but after several unsuccessful attempts, he decides to take legal action.

John presents the signed promissory note to the court as evidence of the debt agreement. Because the note includes all the required elements, such as the amount, interest rate, and repayment terms, the court rules in John’s favor, ordering Mark to repay the loan plus any accrued interest.

The lender can pursue repayment (and collateral repossession, if applicable) via small claims court (a less expensive venue that doesn’t permit attorney representation, thereby eliminating attorney’s fees) for loans under the state limit. Litigation may be necessary if the loan exceeds the lender’s state limit.

Usury is the illegal practice of setting the interest rate on debt (including all extra charges like fees and discount points) higher than the maximum limit set by the relevant law or beyond what’s allowed in an exception to the law. Therefore, usury rates refer to the practice of charging excessively high-interest rates on loans, often exceeding legal limits.

To prevent it, each state has different legislation aimed at limiting the annual percentage rate (APR) a payday lender can charge, depending on the size of the loan, who is making the loan, and loan type.

For example: Sarah, a single mother, faces a financial crisis when her car breaks down, jeopardizing her job and her ability to care for her children. Seeking help, she turns to a recommended private lender who agrees to lend her $2,000 for repairs but imposes an exorbitant 25% monthly interest rate.

Despite struggling to keep up with payments due to the high rate, Sarah is unaware that her state’s usury laws cap interest rates at 10% per month. The lender’s exploitation of her desperate situation violates these laws, plunging Sarah deeper into debt and perpetuating her financial hardship.

In the absence of federal regulation around usury interest rates, each state has its own process for determining the rate, and they may use the following as a baseline:

| State | Maximum Annual Rate | Additional Notes | Law |

|---|---|---|---|

| Alabama | 6%; 8% if agreed upon in writing | Excluding loans over $2,000 | Ala. Code § 8-8-1 |

| Alaska | Federal funds rate + 5%; 10.5% if no contract | Excluding loans over $25,000 | Alaska Stat. § 45.45.010 |

| Arizona | 10%; no limit if agreed and contracted upon | Ariz. Rev. Stat. § 44-1201 | |

| Arkansas | Federal discount rate + 5% (capped at 17%) | Capped at 17% | Ark. Const. Art. XIX § 13 |

| California | 7%; 12% if agreed upon | Cal. Const. Article XV § 1 and Cal. Civ. Code § 1916.1 | |

| Colorado | 8%; 45% if agreed and contracted upon | Colo. Rev. Stat. § 5-12-101 and § 5-12-103 | |

| Connecticut | 12% | Conn. Gen. Stat. § 37-4 | |

| Delaware | Federal discount rate + 5% | Del. Code tit. 6, § 2301 | |

| District of Columbia | 6%; 24% if by contract in writing | DC Code § 28-3301 and § 28-3302 | |

| Florida | Average of the Federal discount rate for the preceding year + 5% | Flo. Stat. § 687.01 and § 687.03 | |

| Georgia | 7%; 16% if contracted in writing and loan is less than $3,000 | No limit if loan is between $3,000 and $250,000 | Ga. Code § 7-4-2 and § 7-4-18 |

| Hawaii | 10% | Haw. Rev. Stat. § 478-2 | |

| Idaho | 12% unless agreed and contracted upon | Idaho Code § 28-22-104 | |

| Illinois | 9% | 815 ILCS 205/4 | |

| Indiana | 25% | Ind. Code § 24-4.5-3-201 | |

| Iowa | 5%; capped at the official usury rate if agreed upon in writing | Iowa Code § 535.2(3)(a) | |

| Kansas | 10%; 15% if agreed upon | Kan. Stat. § 16-201 and § 16-207 | |

| Kentucky | 8%; 19% OR Federal discount rate + 4% (whichever is lower) if agreed upon | No limit if loan is > $15,000 | Ky. Rev. Stat. § 360.010 |

| Louisiana | 12% | La. Stat. tit. 9 § 3500 | |

| Maine | 6%; no limit if agreed upon | Me. Stat. tit. 9-B § 432 | |

| Maryland | 6%; 8% if agreed upon in writing | Md. Code, Com. § 12-102 and § 12-103 | |

| Massachusetts | 6%; 20% if agreed upon | Mass. Gen. Law Ch. 107, § 3 | |

| Michigan | 5%; 7% if agreed upon in writing | Mich. Comp. Laws § 438.31 | |

| Minnesota | 6%; 8% if agreed upon in writing | No limit if loan is > $100,000 | Minn. Stat. § 334.01 |

| Mississippi | 8%; 10% OR Federal discount rate + 5% (whichever is greater) if agreed upon | Miss. Code Ann. § 75-17-1 | |

| Missouri | 9%; 10% OR market rate (whichever is greater) if agreed upon | Only applies to first mortgages made by lenders that are not insured bank, savings and loan, or credit union, or any who have made $1 million in real estate loans in the past year. | Mo. Rev. Stat. § 408.030 |

| Montana | 6% + federal funds rate; 15% if agreed upon in writing | Mont. Code Ann. § 31-1-107 | |

| Nebraska | 6%; 16% if agreed upon in writing | Neb. Rev. Stat. § 45-101.03 | |

| Nevada | Prime rate of NV's largest bank + 2%; no limit if agreed upon | Nev. Rev. Stat. § 99.040 | |

| New Hampshire | 10%; no limit if agreed upon | NH Rev. Stat. § 336:1 | |

| New Jersey | 6%; 16% if agreed upon in writing | - No limit if loan > $50,000 - Interest rates exceeding 30% for loans to individuals (50% for businesses) are considered criminal usury | NJ Stat. § 31:1-1 |

| New Mexico | 15%; no limit if agreed upon | NM Stat. § 56-8-3 | |

| New York | 16% | Interest rate exceeding 25% for loans are considered criminal usury | NY Gen. Oblig. § 5-501 |

| North Carolina | 8%; no limit if agreed upon OR if the loan is greater than $25,000 | NC Gen. Stat. § 24-1.1 | |

| North Dakota | 6%; average interest on treasury bills + 5.5% if agreed upon in writing | [average interest on treasury bills + 5.5%] must be greater than 7% | ND Cent. Code § 47-14-09 |

| Ohio | 8% | No limit if loan > $100,000 | Ohio Rev. Code § 1343.01 |

| Oklahoma | 6%; no limit if agreed upon | Okla. Stat. tit. 15, § 266 | |

| Oregon | 9%; no limit if agreed upon | ORS § 82.010 | |

| Pennsylvania | 6% | No limit if business loan > $10,000 or unsecured notes with loan > $35,000 | 41 Pa. Stat. § 201 |

| Rhode Island | 12%; 21% if agreed upon | RI Gen. Law § 6-26-2 | |

| South Carolina | 12% | SC Code Ann. § 37-3-201 | |

| South Dakota | 12%; no limit if agreed upon | SD Codified Laws § 54-3-1.1 and § 54-3-4 | |

| Tennessee | 10% | Usury rates do not apply for loans under $1,000 | Tenn. Code § 47-14-103 |

| Texas | 6%; 10% if agreed upon | Tex. Fin. Code § 302.001(b) | |

| Utah | 10%; no limit if agreed upon | Utah Code § 15-1-1 | |

| Vermont | 12% | Vt. Stat. tit. 9, § 41a | |

| Virginia | 6%; 12% if agreed and contracted upon | Va. Code Ann. § 6.2-301 | |

| Washington | 12% OR average interest on treasury bills + 4%, whichever is greater | Wash. Rev. Code § 19.52.020 | |

| West Virginia | 6%; 8% if agreed and contracted upon | W. Va. Code § 47-6-5 | |

| Wisconsin | 5%; no limit if agreed upon | Wis. Stat. § 138.04 | |

| Wyoming | 7%; no limit if agreed upon | Wyo. Stat. § 40-14-106 | |

| Show More Show Less | |||

Download a free promissory note template as a PDF or Word file below: